Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

In April 2023 the UK government released its policy paper on gambling reforms for the digital age, and they state their aims clearly:

“At the heart of our Review is making sure that we have the balance right between consumer freedoms and choice on the one hand, and protection from harm on the other.”

The proposed reforms seek to boost the power of the regulators and make operators put better, more effective protections in place for their customers. The UK leads the way in responsible gaming legislation and these reforms look to continue that trend.

The reforms also echo the sentiments of the UK Gambling Commission (UKGC). In their own, accompanying advice paper, UKGC state they have been strengthening their regulatory protections for consumers – and since 2017/18 have issued over £100 million in penalty packages, while revoking ten operator licences.

The policy paper is clear: the UK will expect operators to do more to understand their consumers and protect them from harm. The implications for alternative payments providers like Yaspa that serve the gaming sector are also unambiguous: key sources of this consumer understanding will derive from credit reference style checks … and open banking.

To address problematic play, there are more prescriptive rules about when operators need to check consumers’ financial circumstances. The proposals state that net losses of £125 within a month, or £500 within a year, will trigger more detailed checks.

Data sharing between operators is also proposed in order to identify consumers who have been excluded from other sites. The government is taking inspiration from the financial industry and Credit Reference Agencies as a model of how gambling could be better regulated. The UKGC is now trialling their Single Customer View project, which seeks to share information on at-risk consumers between operators.

The reforms also suggest an array of other changes:

Stake limits are lowered online to between £2 and £15 per spin;

Games that are safer by design;

Introduction of a statutory levy paid by operators;

Closing the gap so that under-18s can do no form of gambling;

Improvements to player-centric tools.

But at the heart of the proposals is the concept that individual operators, and the industry as a whole, need to have more knowledge about their consumers. It is their responsibility to monitor and manage their customers’ activities and reduce gambling-related harm within the context of that consumer’s finances, and possibly in the future within the context of their behaviour across multiple operators. The UKGC would act decisively against operators who do not follow the guidelines.

The reform guidelines state they are walking a tightrope between wanting operators to know more about consumers so that individual protections can be carried out, and introducing draconian policies that will drive consumers away. Asking consumers to produce more documents to prove who they are and demonstrate funds are likely to be counter-productive.

“Industry and racing stakeholders have raised particular concerns that should checks require documents such as payslips or bank statements to be provided to operators, then most people would refuse and instead gamble elsewhere, including with unlicensed operators. Industry estimates based on previous trials are that between 70% and 90% of customers would not comply with requests for such documents to be shared.”

So the government is looking into new solutions: “We recognise this risk, the chilling effect that asking customers for bank documents can have… However, we think the impacts are likely to be mitigated…, [and] most of the checks will be frictionless with little interruption to the customer journey (for instance with credit reference or open banking data replacing the need for documents).”

The policy reform mentions “open banking” four times as a possible solution to create frictionless checks with consumers, and while the government is actively looking at how they can solve their verification issues using open banking, the technology is readily available right now.

Yaspa, which uses instant cardless payments that are backed by open banking technology, is already live and integrated with several gaming operators. With leading online operators, including NetBet and Novibet, welcoming Yaspa as a new payment solution in the UK and across Europe.

With open banking being positioned as part of the government’s solution to verification, it’s worth looking at what other benefits the financial technology can offer to operators.

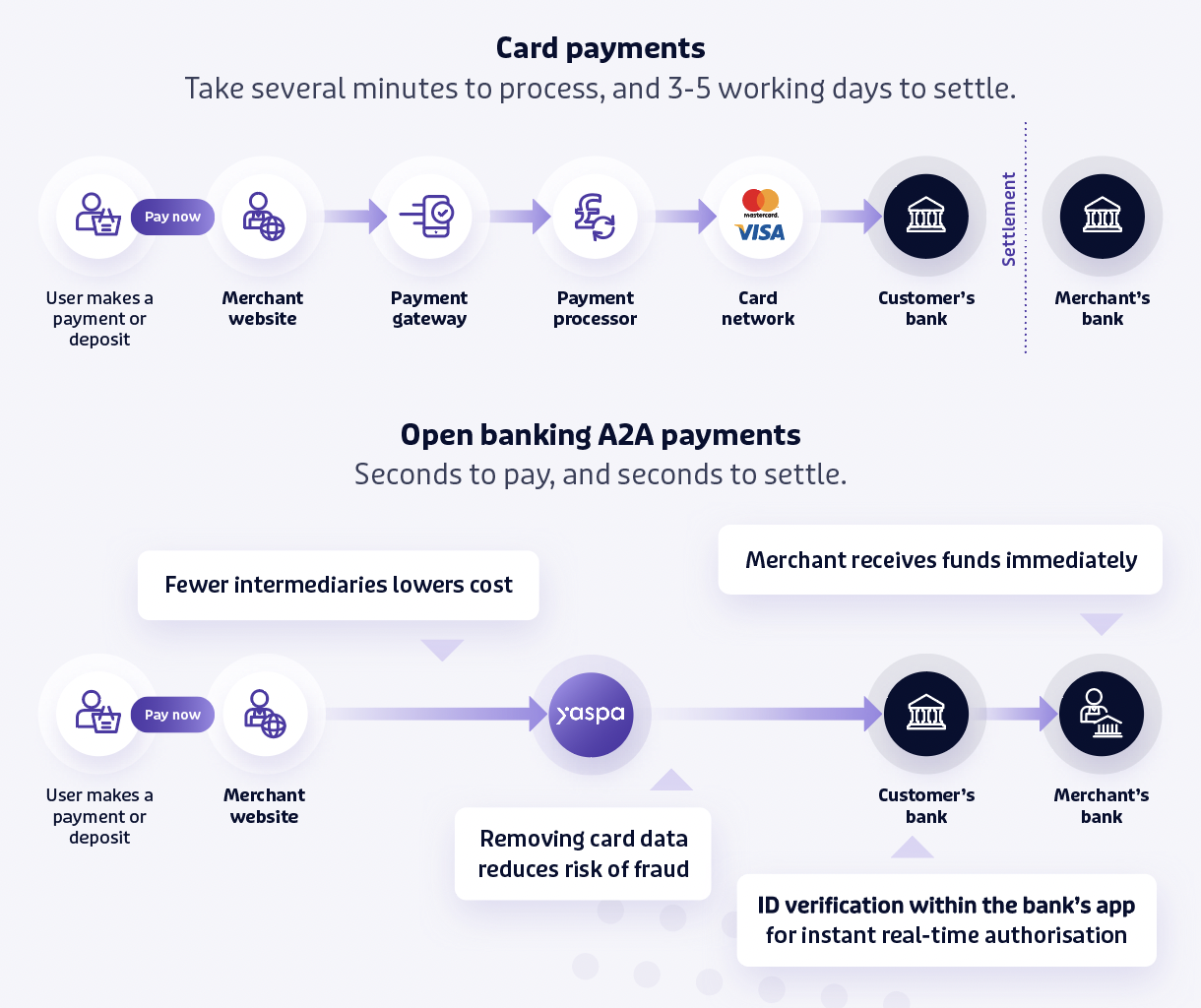

As you can see in the diagram below there are few intermediaries with open banking. These benefits are passed onto the operator in the form of lower fees – as fewer intermediaries (particularly when compared to card processors) means lower transaction costs, as well as payments that settle in seconds.

Depositing using an open banking provider such as Yaspa uses the full breadth of the banks’ authentication mechanisms in the blink of an eye. This is because customers are taken seamlessly to their banking app, with their username, password, facial recognition and two factor authentication (2FA) completely built-in. This process is much more secure than a card deposit, which simply needs the card and minimal personal details about the address.

Additionally, card fraud and chargebacks are massively reduced with open banking, providing operators with greater protection and less support costs to manage problematic cases.

Here is where things get interesting. Open banking is set to bridge the gap between verification and deposits, solving two problems at once:

Now more checks may be needed, but the government has stated they are looking to reform how verification is done generally and they have stated open banking specifically might provide one solution.

It’s often hard to convince a consumer to type their card details into an unfamiliar website. For big trustworthy brands it might be easier, but for smaller operators consumers may be reluctant to share their card details with a site that they might not trust to protect their information.

Open banking solves this problem by setting up payments from the consumer’s banking app directly with the operator, meaning the customer only needs to approve the deposit.

This eliminates the need to trust an operator with a player’s card information and the amount collected, as open banking pushes the deposit from the consumer’s bank to the operator.

Operators invest a lot of effort trying to categorise their players based on their betting patterns and activity to inform marketing strategies and cater to customers’ needs and wants. And it turns out payment mechanisms are also a good indicator of value, and what makes them so valuable is that you can use them to generate an opinion about a customer before they’ve even placed a bet.

There’s a reason for this. Think about fraudulent accounts and bonus maximisers. These individuals use mechanisms built into the payment method itself to take advantage of the operator. Chargebacks on cards can lead to friendly fraud because they make it easy to create hundreds, or even thousands, of accounts with a single operator, enabling individuals to take advantage of bonuses. These fraudulent customers reduce the average lifetime value of that payment mechanism.

With open banking the consumer is using a high security trusted payment mechanism. It’s hard to gain access to someone else’s banking app, let alone create multiple accounts. As such, customers using open banking will generally have a high lifetime value which is advantageous for operators, who can then deploy enhanced payment journeys to cater to and encourage this valuable demographic. At Yaspa we’re obsessed with user experience (UX) so not only is our focus on offering fast and frictionless payments, they’re also a delight to use – with payment journeys built with busy consumers in mind.

Open banking is already an excellent payment mechanism with many advantages over traditional card payments, but with the UK government looking to build it into their arsenal of verification solutions, the offering just gets stronger.

At Yaspa we contend that enhanced verification isn’t a new burden that is being placed on operators as part of this reform, it’s an opportunity to embrace and adopt new financial technologies to verify and understand your customer base from the very moment they register while providing them with the very best payment experience.

Yaspa’s instant cardless payments aren’t just another way to pay, they’re a fundamental part of the relationship with the consumer and protecting them from irresponsible gambling.

Find out what Yaspa has become one of the go-to payment solutions for iGaming businesses across Europe. Try a test payment and contact our team to learn more.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

Sorry, you have reached the maximum number of form entries.