Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

Last month the UK government gave the country’s major banks six months to enable Variable Recurring Payments (VRPs). VRPs will significantly improve the experience of making regular payments for both consumers and businesses.

VRPs are a new concept in finance, introduced in December 2020 by the UK’s Open Banking Implementation Entity (OBIE). At Yaspa, we’ll be offering Variable Recurring Payments through our payment platform as soon as they’re enabled by the banks. It’s worth getting to grips with the basics to understand how VRPs might be able to support your organisation.

Variable Recurring Payments are a feature of open banking, a legal and technological policy being embraced by governments around the world. You can read more about open banking here. In the UK and EU, open banking has created a new type of payments service called a PISP (Payment Initiation Service Provider). PISPs can be authorised by consumers to make payments on their behalf, as is the case with VRPs.

This means that the consumer doesn’t have to manually authorise every payment that needs to be processed on a daily or weekly basis. PISPs are securely connected to the customer’s bank account to make these transactions.

Whenever you hear VRPs being discussed, you‘ll often notice sweeping being mentioned. Sweeping is the regular movement of funds between accounts of the same or different financial institutions in the UK.

At the moment sweeping only enables payments between accounts owned by the same person. It’s mainly used for more effective saving and money management (for example, to move spare funds from your current account into your savings account before payday). In the future, VRPs will apply to accounts owned by a different person or business through the establishment of functions called ‘Trusted Beneficiaries’. This is when it will get really exciting (honest!).

Everything started with the European Union’s second Payments Services Directive (PSD2), which came into force in 2018, setting the foundations for open banking applications. PSD2 was mandated for banks to share consumer data with third-party payment providers (like us) to encourage competition and the development of more innovative products and services.

Both the functionality and underlying technology of VRPs are designed to be simple, with little friction. A traditional one-off payment today can take an inordinate amount of time to process — typically a consumer would manually log their card details, and wait between 24–48 hours for the banks to authorise and transfer the payment. VRPs speed up this process dramatically.

From a regulatory standpoint, VRPs are considered part of a set of payment initiation services provided by regulated Payment Initiation Service Providers (PISPs). A PISP can move funds on behalf of the account holder after it has been provided with ‘explicit consent’. Explicit consent is given through a Strong Customer Authentication (SCA) process — a requirement of the PSD2, which asks businesses to require at least two steps of identity authentication to verify online payments. SCA usually uses biometric authentication (e.g. fingerprints or face ID) which makes it more fraud-resistant and secure for the customer’s payments.

The difference with VRPs is that the consent is ‘long-lived’ so it is consent for payments over a period of time within set amounts, rather than consent for a single immediate payment. VRP consent parameters are fixed rules set by the customer that the PISP must follow when making payments on the customer’s behalf. The customer can set the maximum value of the payments, the maximum number of payments initiated the maximum value of a payment per day/month and the expiry date of the VRP consent.

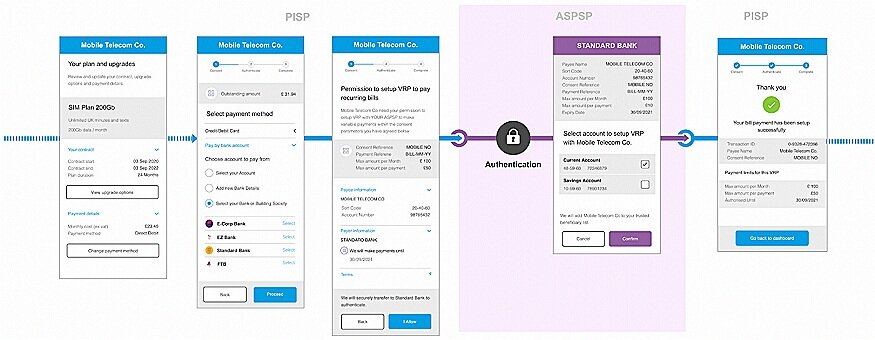

The OBIE envisions that the customer journey for VRPs will work like this:

VRPs should not be confused with Direct Debit payments or standing orders, the regular payment mechanisms most consumers and businesses will be familiar with today. A Direct Debit payment is a transaction occurring between the payer’s account (individual or company) and a business — that is initiated by the business, which pulls the money when agreed from the customer’s account.

Direct debit payments are relatively low cost to the business and easy for consumers to understand, but they still have their challenges:

UK bill payers will also be familiar with standing orders — automated payments that are pushed from the customer’s to the business’s account.

VRPs also rely on push technology but offer more flexibility and control with less friction than Direct Debit and standing orders.

It’s worth noting that VRPs will not immediately displace our current regular payment methods. But in instances where you, as a business, need to take high volumes of payments of varying amounts, VRPs could really make a difference to profit margins and customer churn rates.

Say you’ve set up a meals-on-demand service to which your customers subscribe; but the price they pay each month depends on whether they’ve ordered a salad or steak (or something in between). It would be a hassle for your customers to set up and manage a Direct Debit or standing order, and expensive for you to take cards. With the VRP system, you’ll be able to sign them up easily and process their variable payments each month in a swift and efficient way.

The automation of payments between accounts has numerous benefits for the consumer and businesses.

It’s not just the product teams of companies like Yaspa that will get excited about VRPs in the future. Establishing other parties’ banks as Trusted Beneficiaries will enable us to sweep funds from one bank to another quickly, at a low cost. Any business that takes regular payments will be able to transform their payment processing options.

Variable Recurring Payments are just one of the myriad mini-revolutions occurring in the banking and payments space. If you’d like to talk to us more about how you could make it easier for your customers to pay you, get in touch with us here. We’d be happy to help!

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields