Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

The 2023 Gambling Act White Paper set out a vision for financial risk assessments that would protect vulnerable consumers without disrupting the majority of players. Three years on, that vision is approaching a critical moment. The Gambling Commission has completed its pilot of CRA-based financial risk assessments and is now preparing to present recommendations to its board, with a view to rolling these checks out across the industry. If approved, a joint implementation group with DCMS, operators, and credit reference agencies would be established to develop a rollout plan. The question the industry should be asking isn’t whether checks are coming – it’s whether we’re about to embed the wrong data into regulation.

A quick note on terminology. ‘Affordability checks’ is the historic, broader term used across many industries where spend or lending can be significant. In the gambling sector, it refers to the operator-led process of verifying a consumer can afford to place their bets, often by asking for bank statements, payslips and other documentation. ‘Financial risk assessments’ (FRAs) are the formal mechanism introduced in the 2023 White Paper: checks triggered at defined spending thresholds, and designed to be frictionless by pulling data directly from credit reference agencies (CRAs) rather than the consumer. In practice, there is some overlap in the benefits these techniques provide to identify consumer issues. But the real question is which mechanism provides the best data in real time, without losing the consumer along the way to friction. Yaspa’s solution, by the way, is built to address both points.

To protect consumers sustainably, you need to understand their salary, their disposable income, and their gambling activity across all operators. That’s the open banking proposition – real-time, consent-driven transaction data pulled directly from the consumer’s bank account. One source. One consistent, timely dataset. A clean foundation for building a genuine ‘single customer view’.

CRA data is a different animal entirely. In the UK, three separate agencies – Experian, Equifax, and TransUnion – each independently aggregate information from banks, credit card providers, utility companies, mobile phone networks, buy-now-pay-later providers, debt management agencies, and public records like court judgments and insolvency registers. Not all companies share data with all three agencies, and the data they do share isn’t always standardised. Each CRA then applies its own proprietary models to interpret those inputs. The result is an ecosystem where variation between agencies is structurally baked in.

Even when CRA data is consistent, it tells you the wrong thing. It flags that a consumer has missed payments, entered a debt management plan, or defaulted on credit. In other words, it tells you when the damage has already been done. It’s a rear-view mirror, not a windscreen.

So why did CRA become the mechanism of choice? Because it had one redeeming feature: it’s frictionless. No consumer action required. No consent journey. No drop-off. And that mattered – because the alternative, affordability checks requiring consumers to submit bank statements and personal documents, was failing badly. Industry estimates suggests conversion rates of around 12% at best when consumers are asked for documentation, with 65%* saying they’d refuse outright. Tens of thousands were projected to migrate to unregulated operators. The UK’s black market for online gambling has more than tripled since 2019.

CRA data was never the right answer. It was the path of least resistance at a time when no viable open banking solution existed to solve the consent problem.

If the CRA pilot had delivered clean, consistent results, there would at least have been a small win – a baseline layer of protection, even if it was limited in scope. But that hasn’t happened.

The UKGC’s pilot, running since September 2024 across the UK’s three credit reference agencies, has surfaced exactly that consistency problem in practice: different agencies are returning different results for the same consumer. After 1.7 million checks across roughly 860,000 accounts, there still isn’t sufficient data to explain why.

This is precisely why James Noyes, one of the original proponents of affordability reform at the Social Market Foundation, has called for a pause. His concerns aren’t about the principle of checks – they’re about implementation that isn’t evidence-based, isn’t transparent, and isn’t delivering what was promised.

And this isn’t a UK-only story. In the Netherlands, the Kansspelautoriteit (KSA) has been working through the same growing pains as it tightens deposit limits and affordability requirements: inconsistent data, high friction at the point of check, and consumer drop-off pushing players towards unlicensed operators. The mechanism is the same wherever it’s deployed, which means the answer can be too. A solution that solves the consent and timing problem in the UK solves it across any market weighing consumer protection against conversion.

The reason CRA data was chosen over open banking was simple: nobody had cracked the consent challenge. If only 12% of consumers would engage with an affordability check, the mechanism is dead on arrival – regardless of how good the data is. The problem is that operators ask consumers to complete the check via a standalone email or an engagement message on their website – both operator-initiated actions, disconnected from anything the consumer is actively doing. Consumers don’t complete operator tasks; they complete their own tasks. And beyond the behavioural mismatch, operators face a practical timing problem. When do you send these messages? At what point in the consumer’s journey is the request least likely to be ignored? And if the consumer doesn’t respond, how many times do you follow up before the request becomes irritating or gets filtered out entirely? There’s no good answer, because the mechanism itself is flawed. The check is detached from the behaviour it’s supposed to assess.

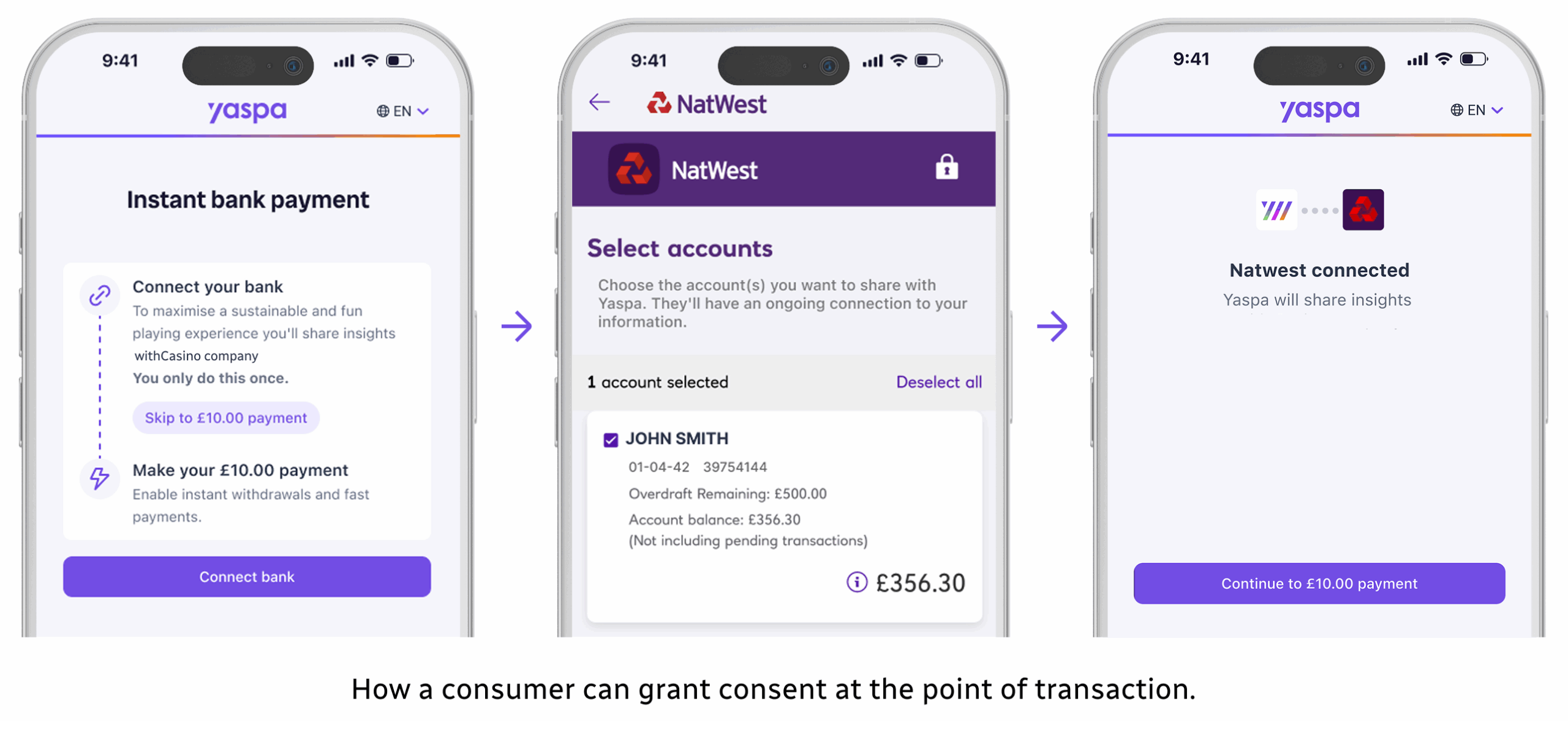

In comparison, Yaspa has developed an affordability check solution and financial risk assessment (FRA) solution that yields a 70% conversion rate in UK trials. This check wins because it ties the check to a customer deposit. The consumer is already mid-action – they’ve chosen to add funds and are actively completing a payment. At that moment, a simple prompt is all it takes: “As part of your deposit, we need to keep you safe by performing an affordability check. Please consent below.” The value is clear, the timing is intuitive, and control remains with the consumer.

Agency bias – People are far more likely to trust a process they initiate themselves. Social platforms deploy this constantly, prompting users to share more only when they’re already taking an intentional action like posting, commenting or updating a profile. This is directly applicable to affordability checks.

Privacy Paradox – the gap between what users claim to care about vs. what they actually do. While many express distrust in how platforms handle data, they still share vast amounts of personal information on Facebook, Instagram, TikTok and beyond. Why? Because when the perceived value is clear – connection, convenience, entertainment – privacy concerns fade into the background.

Yaspa’s approach allows operators to choose, on a per-payment basis, whether to require a check before payment or to let consumers skip it and pay anyway. In UK trials, this flexibility delivered a 70% check conversion rate alongside a 90% payment conversion rate – protection where it matters, without sacrificing the deposit.

In terms of the legislation, Yaspa agrees with James Noyes that a pause is the right call. But it should be a pivot, not a retreat. The original White Paper called for standardised thresholds and independent third-party oversight of consumer data. Those are sound principles – they just need to be built on data that works in real time and a consent model that consumers will actually complete.

The use of credit reference agencies was always a compromise, but now, with open banking technology, a far better solution exists. If you’re exploring ways to integrate affordability checks directly into your payment flow, book a meeting with one of our experts to see how Yaspa’s Intelligent Payments solution can help.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields