Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

The open banking landscape in Ireland is in the early stages of a significant evolution, influenced by domestic legislation and European Union (EU) initiatives. Though current uptake is modest, recent shifts in favour of electronic payments (including contactless, eWallets and alternative methods) indicate a step-change in the way people pay in the country.

Ireland’s payment landscape has shifted towards electronic methods (often referred to as ‘digital payments’), such as cards, eWallets and mobile banking, largely powered by the digitalisation of commerce and widespread smartphone usage by over 90% of the Irish population. Alongside the popularity of debit and credit cards, there’s a noticeable increase in eWallets and contactless payments; the volume of the latter rose to 268.7 million in 2023, hitting three million payments per day (BPFI Payments Monitor Q1, 2023).

The transition to electronic methods is underscored by Ireland’s embrace of domestic digital payments, the number of which has doubled since 2015 due to their convenience and efficiency (Central Bank of Ireland, 2024). However, there’s still room for further advancement, particularly in the adoption of newer payment technologies, such as account-to-account (A2A) payments (the method open banking uses to facilitate transactions) – which is the movement of funds directly from one account to another; and a topic we’ve covered in much more detail in our A2A payments guide.

Ireland has seen a marked change in retail payment behaviour and a rapid shift towards electronic payments. Between 2018 and 2023 the country saw an uptick in digital commerce and is currently ranked fourth highest among EU countries in the proportion of people purchasing goods and services online. Domestic electronic payments rose 150% between 2015 and 2022 thanks to smartphones and mobile banking, and contactless payments comprised 85% of all card-based payments (Central Bank of Ireland, 2024).

The emergence of foreign digital banks offering fast A2A mobile payments in Ireland has also been evident in recent years. Domestic uptake of these kinds of payments has been significant, but not without its challenges (more on this later). This is owing to the ‘unbundling’ or removal of intermediaries from payment chains thanks to new technologies like open banking. When you pay through an open banking provider such as Yaspa, most of the ‘middle men’ are stripped out, resulting in fast transactions without high intermediary costs such as card processing fees.

The growth of electronic and real-time payments in Ireland

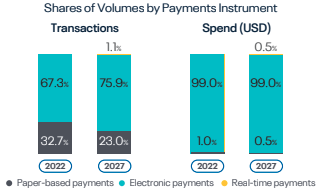

Electronic payments comprised 67.3% of total transaction volume in 2022 (Prime Time for Real Time report, 2023) which creates a promising backdrop for the adoption of alternative payment methods, like open banking-powered payments. The country has already witnessed the gradual but successful rollout of streamlined payment processes like ‘one-click checkouts’, indicating a growing aptitude for new ways to pay. The fact that Ireland is home to many innovative technology companies, including Apple, Google and over 50 e-money institutions, also makes it a promising place for technologies like open banking to flourish.

Despite these advancements, traditional card transactions still dominate, surpassing 1,500 million in 2022, and unlike many of its European counterparts, A2A payments are yet to become widely available in Ireland (Central Bank of Ireland, 2024). Looking ahead, further changes are anticipated in Ireland’s payment landscape, driven by continued innovation and technological advancements in the payments industry.

Simply put, open banking allows secure access to bank-held customer data and there are plenty of reasons to pay with it, including its ease of use, speed and security. You can read about it in more detail in our extensive article, What is open banking?

Ireland is part of the Single Euro Payments Area (SEPA) initiative, which enables anyone with a bank account to send euro payments to and from accounts located elsewhere within the SEPA – known as a SEPA Credit Transfer (SCT). Despite this, there has been no uniform implementation at the national level in Ireland of the real-time payments service housed within this initiative (and powered by open banking technology), called SEPA Instant Credit Transfers (SCT Inst). The outcome is that only a small number of Irish banks currently offer SCT Inst.

The absence of universal implementation standards means that open banking in Ireland still faces some significant barriers to success.

In the UK a new entity was established, Open Banking Limited (OBL), for the express purpose of standardising the implementation of open banking in the country post-PSD2 (a directive designed to improve payments and secure data sharing in the UK and EU). But Ireland is yet to implement a standard implementation framework.

Contrasting compliance rules have prevented the development of an agreed way to effectively ‘turn on’ open banking APIs (the interfaces developers use to connect software applications) in Ireland, both for payment institutions, like banks, and third party providers (TPPs), stifling its roll-out. This also impacts what data is shared with TPPs, and how. Without an agreed framework the ability to vet or control user data is diminished, resulting in security risks that impede the effective implementation of open banking in the country.

The lack of standardisation in Ireland has also resulted in a form of bank account – or IBAN – discrimination. In the case of Ireland, this is where transactions or direct debits made using an IBAN from a jurisdiction outside of the country are treated as international payments, rather than a domestic SEPA payment, imposing friction-inducing mechanisms that make the payment more difficult.

This is the case for AIB, one of Ireland’s largest banks (which holds a 33% share of the market). AIB doesn’t allow users to make payments to and from an Irish bank to an IBAN registered overseas without employing a card reader. This is a problem because it creates a huge amount of friction for the user, undermining the very point of making a payment using open banking – to facilitate instant, frictionless transactions that are cardless by definition. It can also impact people making domestic payments from AIB to another Irish bank account using non-native payment services, like digital wallets or open banking providers, whose banking infrastructure (including their IBANs) is based overseas.

TPPs that provide open banking payments, like Yaspa, have had to come up with clever and innovative workarounds to address IBAN discrimination. At Yaspa, for example, we include a pop-up within our Irish payment journey that warns users in advance that they’ll need their card reader and directs them instead to banks with a higher conversion rate. This allows users to select an alternative bank, such as Wise or Revolut (who together hold a 35% market share), which guarantees a more seamless experience and instant settlement.

In the absence of an agreed way to implement real-time payments infrastructure, a handful of the country’s largest banks (by market share) are yet to offer SCT Inst through open banking, meaning payments to these banks won’t necessarily settle instantly. This being said, these banks still provide instant payment outcomes (whether a payment has been ‘accepted’ or ‘rejected’ by the bank) making it a reliable way to pay despite the slow settlement. However, thanks to legislation announced by the European Parliament in February 2024 – which mandates that all transactions within the Eurozone take less than 10 seconds – this issue will soon become obsolete. This legislation forms a part of a wider plan to regulate and standardise real-time payment infrastructures across the EU, which will undoubtedly benefit open banking in Ireland.

Ireland’s payments landscape is evolving quicker now than ever before. The legislation introduced by the European Parliament – regulating and expediting the provision of real-time payments to consumers – is likely to be the largest driving force of open banking’s adoption in the country. Because of the disparity in access to open banking services to date, Ireland stands to benefit from the regulation exponentially compared to its fellow EU members. In short, we can expect a marked shift in the availability and improvement of open banking services (including real-time payments) within the next few years.

Yaspa is at the forefront of the open banking revolution. We offer a wide range of services including:

If you’re interested in learning more about what Yaspa can do for your business, do get in touch. We would love to hear from you.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields