Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

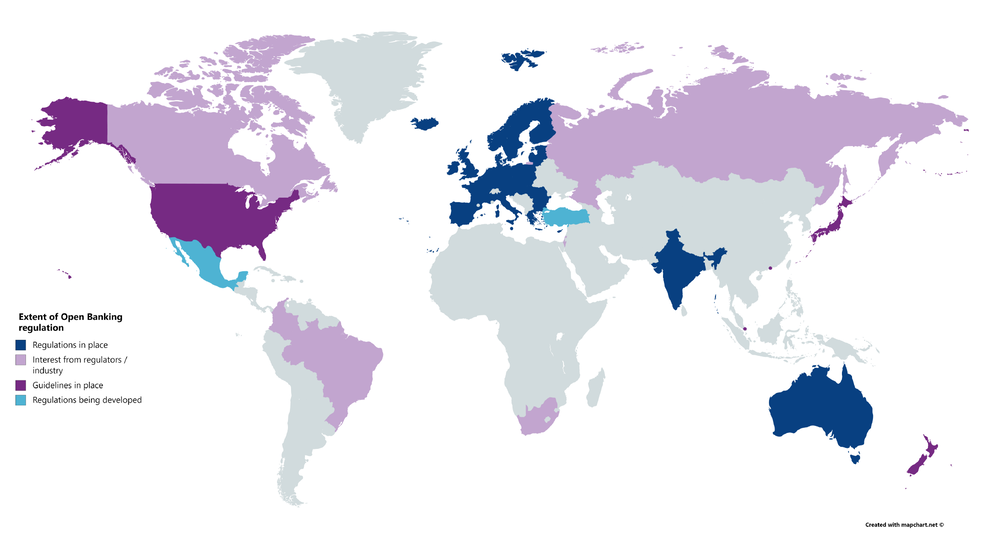

Open banking provides third party companies (like Yaspa) free, permission-based access to customer’s bank account data to develop and improve a wide range of innovative and useful products and services.

It is based on the idea that open, consensual access to consumers’ bank account data benefits them and supports competition in the market. Traditionally, banks have been data silos – lacking an incentive to let other companies access their customers’ information. But now regulators across the world are working to free up access to this data for the sake of competition and innovation.

Instant third-party access to customer bank account data supports the development of new services and thriving fintech ecosystems. From a consumer perspective, this means easy access to a range of new and improved financial services, from budgeting apps to loans.

Application Programming Interfaces (APIs) are the technology at the heart of open banking. If Banks provide standardised APIs to share customer account data, they make it possible for Third Party Providers (TPPs) to offer products and services based on direct access to that data.

It’s like ensuring each bank has a standard-shaped lock on its door; the data is still secure, but it’s easier for a trusted third party to work with multiple different banks to get access, rather than having to start from scratch each time.

The EU’s PSD2 legislation has given open banking momentum in Europe — it’s the foundation for simple and secure data sharing between banks, consumers and third parties, and other authorities are driving similar programmes across the world.

Open banking works by allowing licensed third-parties to securely access a user’s financial data like bank account transactions and details, with the user’s explicit consent, and through the use of open APIs. It’s these open banking APIs which allow the payment initiation capability.

So when a payment is initiated via an open banking API, typically by a licensed third party provider (TPP), like Yaspa, to a bank, the instruction is to move money through the faster payment rails to facilitate the bank account-to-account transfer. These faster payment rails (e.g. FPS in the UK, and SEPA Instant in Europe) are the infrastructure that enables real-time money transfers between bank accounts.

The Payment Services Directive 2 (PSD2) came into effect for EU Member States on 13 January 2018, when states had to transpose it into national law. It was designed to create a Digital Single Market for payments in the EU.

The directive focuses on making payments safer for consumers and promoting competition and innovation in financial services. This is achieved by improving security standards for payments and requiring banks to provide APIs for Third Party Providers (TPPs), making it easier for new fintech companies to provide their services securely. The directive applies to bank accounts held by people in each of the EU’s member states and the UK.

PSD2 created two new kinds of company; Payment Information Service Providers (PISPs) and Account Information Service Providers (AISPs). Both require direct access to consumer bank accounts, with their consent. AISPs access account data like account holder information and transaction history, useful for budgeting apps, credit assessments, and proof of identity. PISPs can initiate bank-transfer payments directly from the payer’s account, with their authority. As outlined above, these open-banking payments settle instantly, incurring no interchange fees or card infrastructure charges.

TPPs can be licensed as either a PISP, AISP or both. Once regulated by the appropriate authority, they can connect their applications to the banks’ APIs. This will usually involve collaboration with their national or regional implementation organisation. In the UK, this organisaton is named Open Banking Ltd (OBL). The OBL, formerly known as the OBIE, has helped develop industry standards, build supporting infrastructure, drive adoption of open banking within the UK and much more.

The are plenty of benefits when it comes to open banking:

There are plenty of reasons why open banking is a safer alternative to traditional payment methods:

And yes, that in turn means it’s also safe to pay with Yaspa too.

Not all banks were ready with fully usable APIs when PSD2 was first introduced, and whilst it’s not perfect, things have progressed considerably over the last few years, and bank API and payment processing standards improve daily. PSD2 is the foundation for intra-European payment and account information services. Lower payment fees, consensual access to consumer account data and EU-wide standardisation will open and connect financial services at an unprecedented scale. So, what else can we expect?

The European Commission has since proposed updates to PSD2. The new directive, PSD3, along with a new Payment Services Regulation, aim to modernise and amend the existing framework. As a regulated payment provider compliant with PSD2, at Yaspa we are well-positioned to guide clients through these upcoming changes and provide continuous service during the transition. You can read more about this in our blog on PSD3 here.

A number of upcoming features add to the adaptability of the initiative, particularly expansions to the payment capabilities of PISPs. These include trusted beneficiaries, reverse payments and variable recurring payments.

Yaspa is at the forefront of the open banking revolution. We facilitate instant bank payments and account verification via open banking technology.

With Yaspa instant bank payments, you get real-time settlement and none of the fraud risk that comes with cards. Our focus is on developing a product that’s easy to integrate and operate, with an excellent end-customer experience. We’ve tested and improved our payment flows extensively, making sure they’re as quick, clear and intuitive as possible.

With Yaspa account verification, it makes it easier to onboard new customers as well as pay refunds and withdrawals to customers. Verifying customer accounts via open banking removes the need for them to submit paper statements, make microtransactions or use authentication codes. Customers approve verification requests directly in-app, a more secure process that leaves no room for fraudulent submissions.

Our full range of services including:

If you’re interested in hearing more about what Yaspa can do for you, get in touch with us and our team will get back to you as soon as possible.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields