Faster checkouts. Safer payouts. Happier customers. We design payments around people, not processes. Blend biometric ID, instant settlement, and a seamless experience into one, frictionless flow.

How it works

Insights that let you see

the bigger picture

Guaranteed payments

ACH-guaranteed pay-ins

Instant payouts

High approval rates

Low return rates

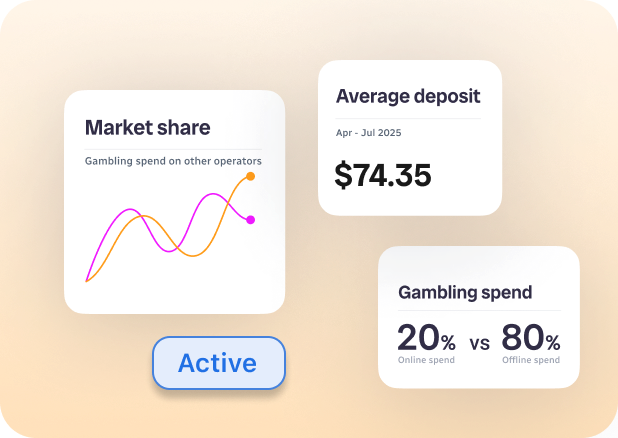

Real-time insights

Cross-operator transactions

Financial resilience signals

Dynamic income categorisation

Real-time spending behaviour

Fast and friction-free

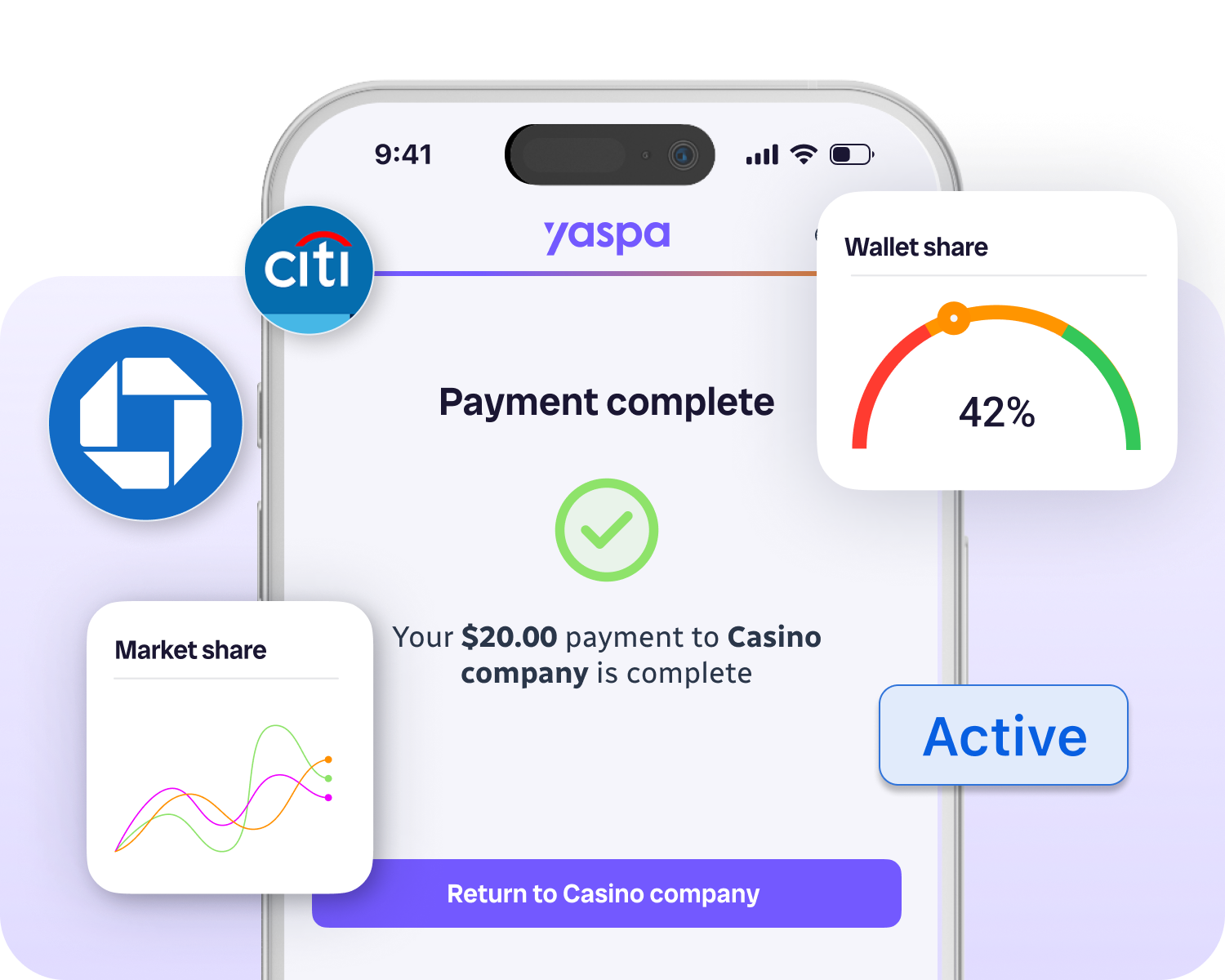

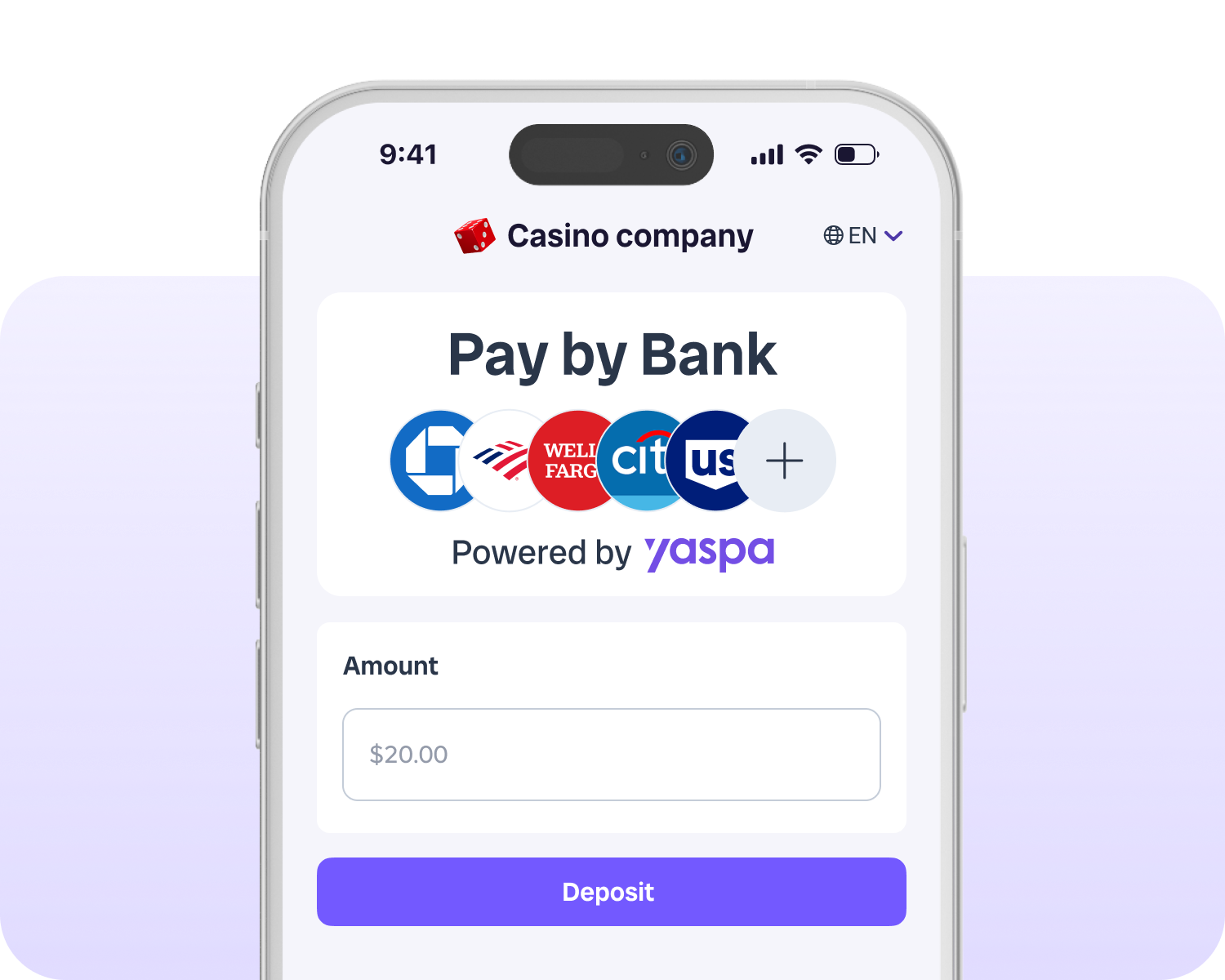

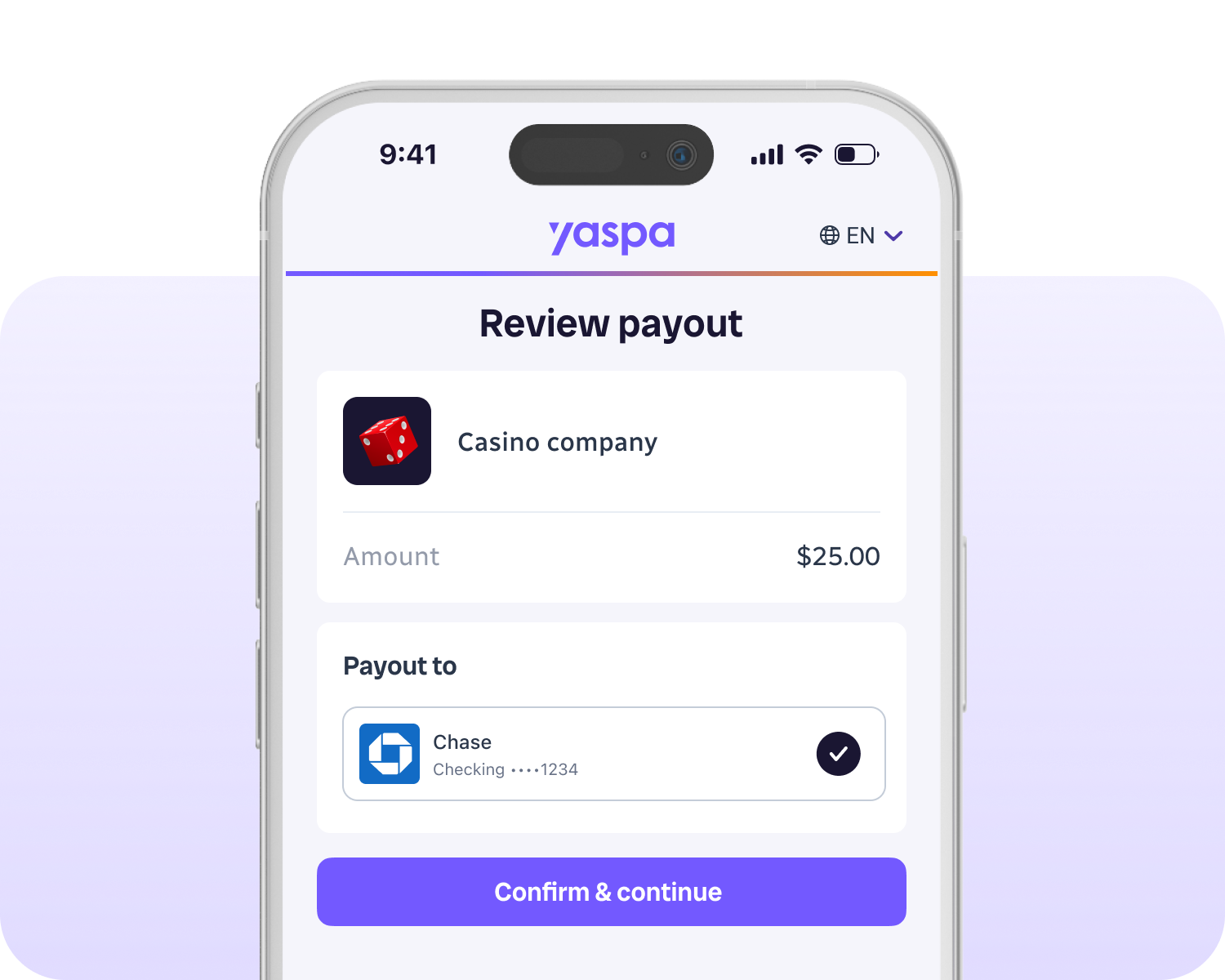

From deposit to withdrawal, Yaspa delivers seamless Pay by Bank with real-time approvals, guaranteed protection against returns, and instant RTP payouts.

Intelligence that keeps you ahead of the game

Yaspa’s intelligent infrastructure constantly adapts, surfacing insights, streamlining reconciliation, and keeping you one step ahead.

Trust in every touchpoint

With biometric verification and zero fraud tolerance, Yaspa wraps every transaction in enterprise-grade protection, without slowing you down.

Turn every payment into a moment of clarity. Yaspa unifies identity, insight, and innovation, giving you real-time actionable intelligence without adding complexity.

Our products

Payments that flex to fit your world

Intelligent Payments

Guaranteed payments.

Responsible intelligence.

Make smarter decisions from the first deposit. By blending ACH guaranteed payments with cutting-edge AI, Yaspa delivers player intelligence like you’ve never seen before.

Guaranteed Payments

Built for simplicity.

ACH guaranteed.

Guaranteed outcomes for operators. Faster approvals for players. Powered by live balance checks and guaranteed deposits across Same-Day ACH, from checking and savings accounts.

Instant Payouts

Withdrawals that don’t keep users waiting

For refunds, withdrawals and outbound payments that settle instantly.

Account Verification

Verify who’s behind the payment – instantly

Verify players in seconds with

real-time account ownership

checks for fast, frictionless KYC.

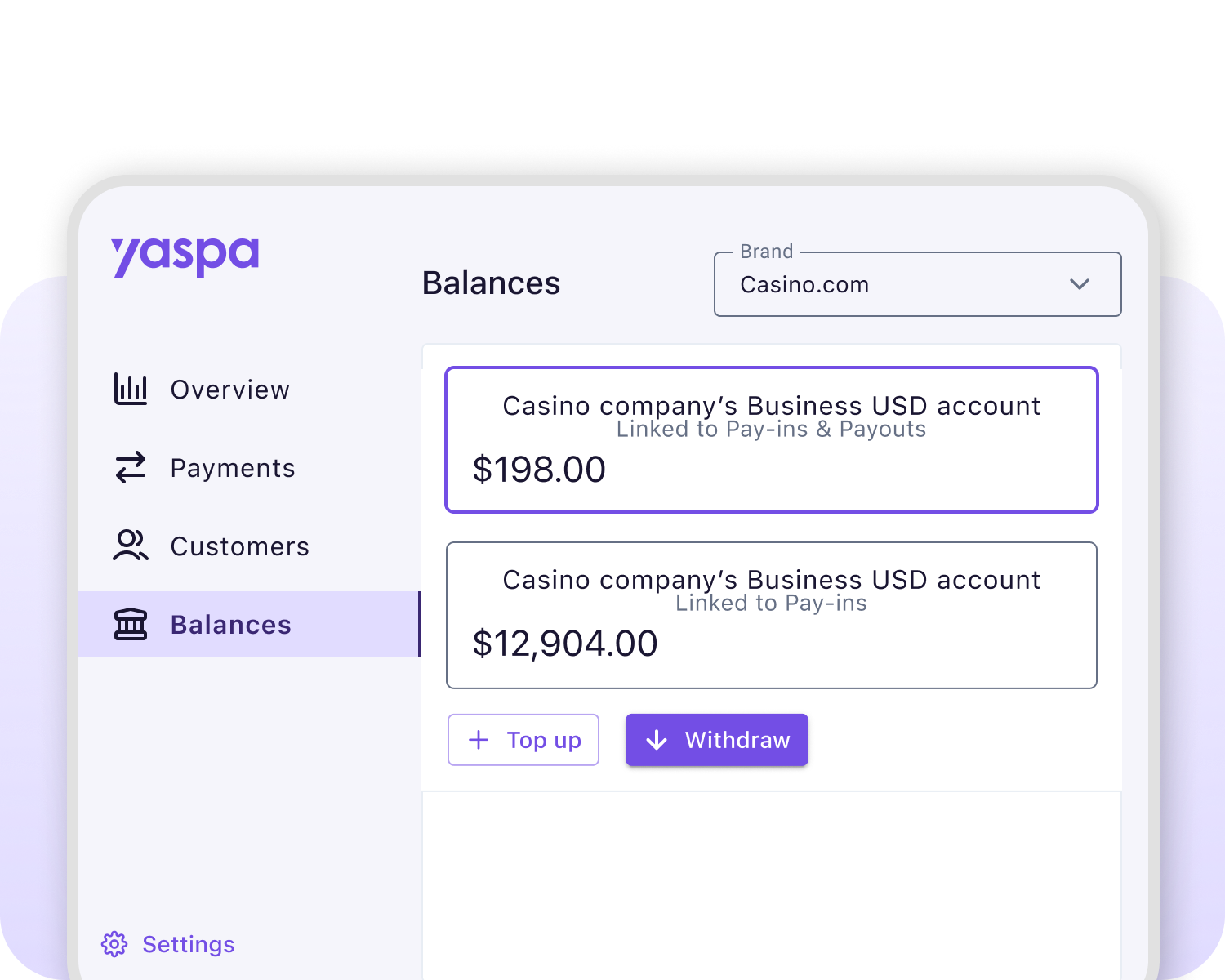

Virtual Accounts

Track, split, or reconcile payments with precision

On-demand corporate holding accounts for simple funds management, instant payment outcome and reconciliation.

Luke Cousins

Commercial Director at Playbook Engineering

”A huge thing for me was the people involved in the business… people you actually want to spend time with and communicate with. And Yaspa massively ticked that box.”

“Yaspa added huge value in making onboarding and withdrawals seamless—crucial battles in our industry.”

Fivos Polymniou

Director at Ask Global Solutions

“Our partnership with Yaspa reflects our commitment to provide cutting-edge payment solutions that enhances both operational efficiency and customer experience. By integrating open banking into our PINTO kiosks, we are further cementing the freedom of our customers to choose the payment solution that works for them.”

Nikogiannis Karantzis

CEO and Managing Director, ISX Financial

“Our partnership with Yaspa marks a significant milestone in expanding instant payment capabilities across Europe. We are focused on innovating the way businesses transact, offering seamless, secure, and real-time payment solutions tailored to meet the diverse needs of our clients.”

Paolo Sanvido

CEO of Casino Lugano

“We are pleased to welcome Yaspa as an innovative payment method at Casino Lugano. With Yaspa, we are excited to offer more and more services with solutions that simplify the payment experience for our Italian guests, making the gaming experience even more comfortable. Partnering with Yaspa is a great opportunity to keep adapting to change and fully meet the demands of our customers.”

%

Average conversion rate

%

Average return user rate

X

Faster than cards

Get started

Let’s make payments work

for you

European iGaming Awards

Best Payment Solution Provider 2026

Open Banking Expo

Best Use of Data – Consumer 2025

Payments Awards

Real-time Payments Innovation 2025

Hyer

People’s Platform Award 2023

Welcome to the Jungle

Fintech’s Finest 50 List 2025

Open Banking Expo

Best Open Banking Payments Project 2023

Innovate UK

UK Innovation Grant 2024

SBC Awards Europe

Silver – Payment Solution of the Year 2025

SiGMA Europe B2C Awards

Best Innovation in Responsible Gaming 2024

The Card & Payments Awards

Best Payment Facility 2025