Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

Open banking is thriving in the United Kingdom – it’s deployed well and usage is growing month-on-month:

Open banking has been driven by the EU’s Payment Services Directive 2 (PSD2), and enables secure access to customer financial data held by banks through open application programming interfaces (APIs) to authorised third parties. Open banking comprises both AIS (account information service) and PIS (payment initiation service) features. Open banking payment initiation services facilitate real-time account-to-account payments, from one account bank to another, typically processed through the payer’s mobile banking app.

Simply put, an open banking payment should be:

1. Fast to settle.

2. Simple to transact.

3. Secure.

We’ve written an extensive article on the topic of what open banking is, and you can read more about that here.

The B2C payment landscape in the UK is diverse, featuring traditional methods like debit/credit cards alongside newer alternatives such as cryptocurrency, Buy Now Pay Later (BNPL), and open banking. Contactless payments have gained widespread popularity, with contactless cards and mobile payment wallets like Apple Pay and Google Pay becoming integral to everyday transactions. Mobile banking apps have become essential tools, providing users with convenient access to manage finances and conduct transactions through smartphones.

*Faster Payments refers to open banking payments

For more information on alternative payment methods (APMs), including open banking, you can read our report here.

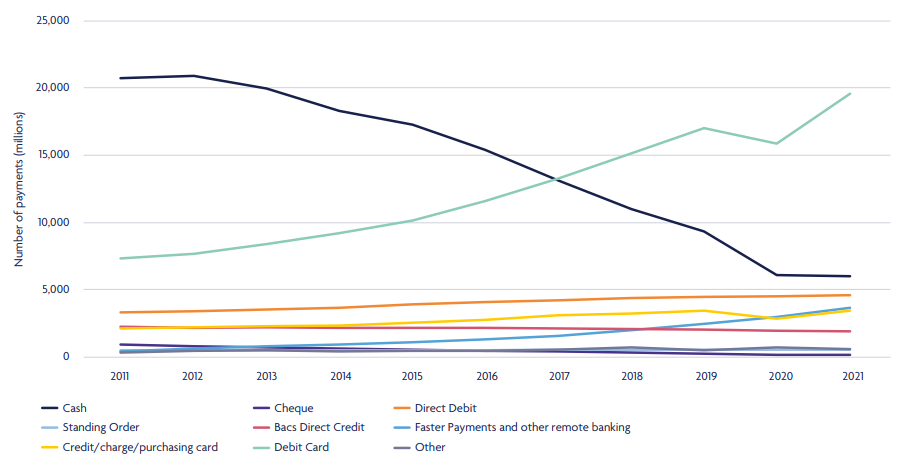

The UK payments landscape is rapidly digitising, with contactless payments now accounting for over a third of card transactions and nearing 90% consumer adoption. Mobile payments are also rising swiftly, with 47% of adults using their device to make payments (The Financial Lives Survey, 2022). However, merchant dissatisfaction persists over the cost of card acceptance, which has seen scheme fees rise 28% recently.

Moreover, card fees are complicated – that’s because there are various fees attached to card payments, such as the authorisation fee, terminal charges, merchant service charge (MSC), Payment Card Industry (PCI) compliance fee, gateway fee and other additional administrative fees. We should mention here that this isn’t the case with open banking, which is much simpler.

Looking ahead, continued growth is expected in real-time/Faster Payments enabled transactions underpinning innovations like open banking.

Open banking adoption in the United Kingdom continues to accelerate, with active user growth increasing to 11% of consumers as of October 2023, up from 7% in December 2021. The number of open banking payments also climbed, reaching 10.8 million transactions in August 2023. The country currently ranks 17th globally in real-time payment transaction volume per capita.

The UK’s Open Banking Ltd (OBL) has been instrumental in spearheading the rollout of open banking across the UK. The OBL (formerly the Open Banking Implementation Entity (OBIE)) has helped develop industry standards, build supporting infrastructure and drive adoption of open banking. The OBL was set up by the nine largest retail banks in the UK (CMA9):

Another factor in the rapid uptake of open banking within the UK is its infrastructure – or ‘payment rails’ – with one notable component being the Faster Payments Service (FPS). FPS is a near real-time electronic payment clearing system that enables same-day sterling transfers between UK banks.

Elsewhere, regulatory oversight from entities like the Financial Conduct Authority (FCA) ensures the industry’s adherence to fair competition and consumer protection standards. The Joint Regulatory Oversight Committee (JROC), which is led by the FCA and the Payment Systems Regulator (PSR), is responsible for overseeing the next phase of open banking in the UK. Their roadmap focuses on expanding availability, mitigating financial crime risks, strengthening consumer protection, improving information flows, as well as launching a variable recurring payments (VRP) pilot scheme later this year.

The Crown Dependencies including Jersey, Guernsey and the Isle of Man are not part of the UK or EU and their local banks have not yet opened up to open banking.

It’s important to reiterate that the UK is well set up for open banking, with its usage continuing to grow. The technical infrastructure is good, and bank APIs are reliable. As one of the leading open banking providers in the UK, Yaspa regards adoption challenges more on the consumer side:

1. Consumer familiarity

2. Consumer confidence

Currently, there are many providers of open banking services, including Yaspa, with varied symbols and messaging (‘cardless payments’, ‘pay by bank’ etc). We expect to see this converging over time so that consumers will be able to click on an open-banking provider with the confidence that they’ll understand the payment mechanism they’re about to use.

Consumers may also be concerned about access to their bank account data, so it’s important to remember that access is always consent-driven and this may be withdrawn at any time by the consumer via their bank. Consumers now only need to provide their account information service provider (AISP) with reconfirmation that they consent to having their data accessed.

Open banking payments are fast, secure and easy for consumers to make, and equally convenient for merchants to receive and process – with real-time settlement; cost-effective charging; and pay-in, payout and VRP options. We’re just at the start of this growth.

The state of open banking in the UK reflects a dynamic and evolving landscape. The payment ecosystem is diversifying, with open banking playing a pivotal role in shaping the future of financial transactions. As technology continues to advance and consumer preferences evolve, the UK’s journey through open banking promises continued innovation and transformation in the financial realm.

Yaspa is at the forefront of the open banking revolution. We offer a wide range of services including:

If you’re interested in learning more about what Yaspa can do for your business, do get in touch. We would love to hear from you.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields