Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

The Netherlands Gambling Authority (KSA) has drawn a clear line: self-declarations, plausibility checks, and questionnaires are no longer acceptable methods of verifying a player’s income. If you’re a Dutch-licensed operator still relying on any of these, your affordability process isn’t compliant.

This isn’t a future concern. The KSA’s Financial Capacity Assessments: Duty of Care guidance – published alongside its 2026 supervisory agenda – spells it out explicitly. And the fines already being handed down show the regulator means it.

In October 2025, the KSA fined BetCity €2.65 million for failing to protect young adults from gambling harm. The investigation examined 10 players aged 18 to 23 who had collectively deposited more than €500,000 over a short period. The regulator found that BetCity either responded too late – or not at all – to warning signs of excessive play.

Two months later, LeoVegas received a €500,000 fine after an eight-month audit uncovered compliance gaps in every player file reviewed. In one case, a player lost tens of thousands of euros without timely intervention.

KSA chair Michel Groothuizen was unambiguous: “We have intensified our oversight of the online duty of care, and we are taking strong action against violations.”

The message to operators is clear. Duty of care isn’t optional, it isn’t aspirational, and the KSA is actively auditing player files to check compliance.

The KSA’s good and bad practices guidance sets out the specific standard operators must meet when assessing a player’s financial capacity.

To increase a player’s net deposit limit beyond the default thresholds – €700 per month for adults, or €300 for young adults aged 18 to 24 – operators must conduct a financial capacity assessment based on verifiable supporting documents. The information must be sufficient, accurate, and verifiable.

What doesn’t meet this standard:

The KSA’s position is that increasing a player’s net deposit limit based on this type of information “is not permitted.”

Beyond the verification standard itself, operators must also get the underlying calculation right. Borrowed money, earmarked income (child support, personal care budget, housing allowance, insurance benefits, tax credits), partner income, and business expense reimbursements must all be excluded. Liquid asset receipts – savings transfers, one-off gifts, gambling withdrawals – are not income. Non-liquid assets like home equity or business equity can’t be counted either.

Get the calculation wrong, and it’s a compliance breach.

The problem with manual income verification isn’t just that it’s slow – it’s that it creates friction at exactly the point where operators can least afford it.

When a player hits a deposit threshold, the traditional process looks something like this: the operator sends a request for documents (payslips, tax returns, bank statements), the player receives the request, and in most cases, they don’t respond. In the UK market, Yaspa has seen drop-off rates for document requests exceed 80%. Players don’t stop gambling – they go somewhere that doesn’t ask.

In the Netherlands, where channelisation remains a live concern, this is a commercial problem as well as a compliance one. Every layer of friction in the verification process risks pushing players towards unregulated operators who don’t ask questions at all.

And even when documents are submitted, the process isn’t straightforward. Tax returns need to be interpreted correctly – the KSA has flagged operators who calculated net income by subtracting the wrong field. Self-employed income needs careful handling: gross dividends and balance sheet assets are not net income, a mistake the KSA has observed multiple times.

Manual document review is slow, expensive, error-prone, and bad for player retention. It’s also no longer the only option.

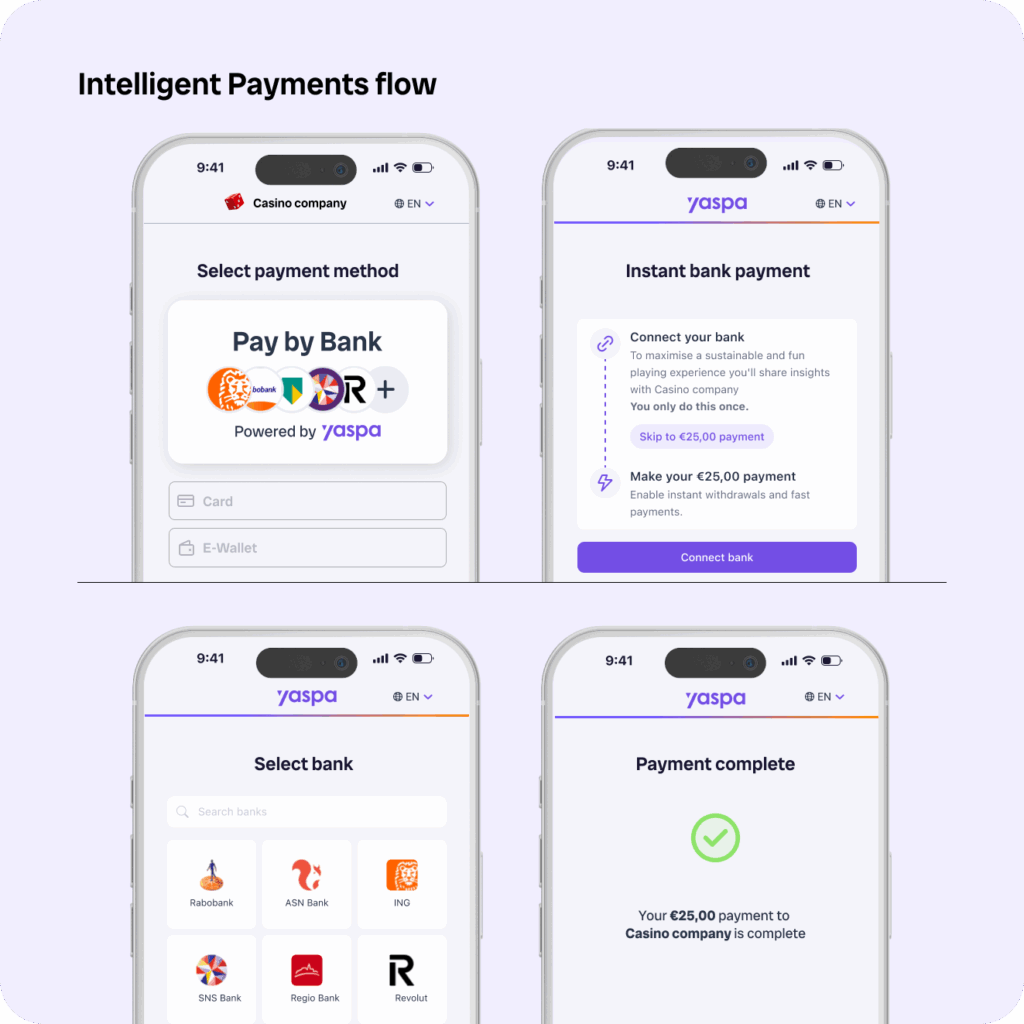

Open banking offers operators a fundamentally different approach to income verification – one that’s faster, more accurate, and invisible to the player.

Here’s how it works: when a player makes a deposit via open banking, they connect to their bank through secure biometric authentication. With their explicit consent, the operator gains read-only access to their transaction data. From that single connection, income can be verified directly from the source – not from a document the player uploads, but from the bank data itself.

This isn’t a one-time snapshot. Under current EU standards, open banking consent lasts 180 days, meaning operators receive a continuous feed of transaction data that keeps affordability assessments current. If a player’s financial situation changes – a salary stops, new loans appear – the operator can see it in real time.

For the KSA’s requirements specifically, open banking data is stronger evidence than a static payslip or tax return. It’s live, it’s verified by the bank, and it’s timestamped – making it inherently auditable.

Yaspa’s Intelligent Payments platform is built to turn this open banking data into actionable compliance intelligence at the point of payment.

When a player deposits, Yaspa’s AI transaction categoriser analyses their bank feed and identifies income automatically – recurring salary inflows, employer payments, benefits, dividends – with 95%+ accuracy on known merchants. This isn’t a generic categorisation; Yaspa’s models are specifically tuned for the financial patterns that matter to iGaming operators.

What makes this particularly relevant for the Dutch market:

The player experience is frictionless: they connect their bank once during the deposit flow, and the compliance check happens in the background. No document uploads, no questionnaires, no waiting. For the operator, the result is a verified, timestamped, audit-ready assessment that resolves in under 30 seconds – compared to the days or weeks a manual document process typically takes.

It’s worth stating plainly: evidence-based income verification isn’t just a compliance requirement. It’s a retention strategy.

Players asked to upload payslips don’t tend to stick around. Players who connect their bank via open banking – a process that takes a few taps and feels like a normal payment step – tend to stay. Operators using Intelligent Payments have seen significant improvements in VIP retention compared to manual source of funds processes.

The same data that keeps operators compliant also unlocks commercial insight. Verified income data reveals players with high disposable income and low gambling spend – hidden VIP opportunities that manual checks would never surface, because those players would never have submitted their documents in the first place.

For Dutch operators navigating the KSA’s tightened rules, the question isn’t whether to move to evidence-based verification – the regulator has already decided that. The question is whether to do it in a way that adds friction or removes it.

If your current affordability process relies on questionnaires, self-declarations, or manual document review, it’s time to reassess. The KSA’s position is clear, the fines are real, and the first wave of licence renewals arrives in October 2026.

Yaspa’s Intelligent Payments platform is already helping operators across Europe, KSA licensed operators in the Netherlands, meet stricter affordability requirements without compromising the player experience. To see how it works for the Dutch market, talk to one of our experts.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields