Everything you need to know about payment gateways

Yaspa

What is a payment gateway? Is it the same with a payment processor? How does it work and how do I choose one for my online business?

If you’re a small business owner looking into digital payments for the first time, it’s very easy to get lost in all the jargon. So, here’s a quick glossary of key terms:

Payment gateway: a payment gateway is a business that captures and transfers payment data from the consumer to the acquirer or payment method.

Payment method: a payment method is a way for customers to pay for products and services. In physical stores, these may include cash, gift cards, credit/prepay/debit cards, or mobile payments. Online these may also be e-wallets and credit financing such as Buy Now Pay Later (BNPL) methods such as Klarna.

Cardholder: the person who is making the payment (the consumer).

Card network: a company that provides credit and/or debit cards (e.g. Visa, Mastercard).

Card issuer: a financial body that offers cards and credit limits to consumers.

Acquirer: a financial institution which processes credit/debit card transactions on behalf of the card issuers.

Issuing bank: the cardholder’s bank, processing payments on the consumer’s behalf (typically sending funds to the merchant).

Acquiring/Merchant bank: the bank that is processing payments on behalf of the merchant (receiving funds from the consumer).

Merchant: the business that is accepting the payment (e.g. a retailer).

What is a payment gateway?

A payment gateway is a payment services provider (PSP), such as a bank or another financial institution, that offers online and offline payment technology to merchants. Previously, payment gateways only accepted credit and debit card transactions, but now with a plethora of alternative payment methods (APMs) available, payment gateways can process both traditional forms of payment – such as cash, cheques and cards – as well as BNPL, tap-and-pay, cross-border and account-to-account (A2A) payments (like Yaspa).

How does a payment gateway work?

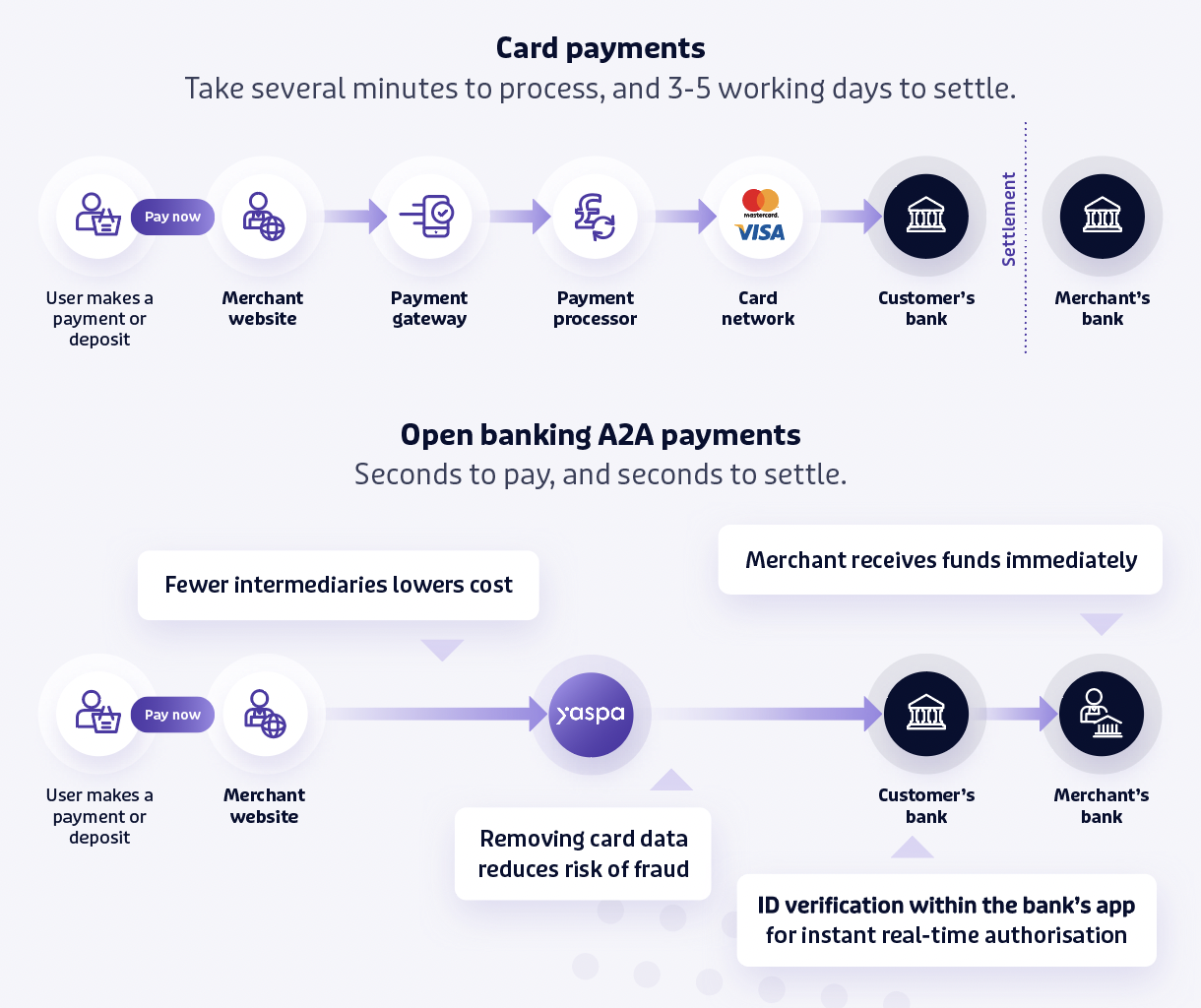

When a cardholder makes a payment on an online or offline store, the payment gateway reads and captures the information about the payment.

Next, the gateway forwards the information to the acquirer or payment method (“payment processor”).

The payment processor contacts the issuing bank to confirm that there are enough funds for the payment to be processed without compromising the cardholder’s balance.

Then the payment processor contacts the card issuer to initiate and process the transaction to their acquiring account.

The payment processor then responds when the money has been transferred successfully.

The payment processor settles the funds to the merchant either daily/weekly or some other pre-contracted timeframe, minus their fees.

That’s a lot of players, and it’s a super complex process. That makes it time-consuming, and expensive. In contrast, see how simple an open banking payment is when compared to a card payment:

Payment gateway vs. payment processor

A payment processor is a company that acts as an intermediary between the merchant and the banks, overseeing the payment process from data collection to funds settlement. It’s employed by the merchant to supervise their transactions. Card networks like Visa and Mastercard (which are also issuers) are good examples of payment processors because they, quite literally, process the payments that go through them.

So, if a payment gateway is employed by a merchant and is processing payments on their behalf, doesn’t this mean they are a payment processor?

Not necessarily. Payment gateways handle the front-end of a transaction between the cardholder and the merchant, while payment processors focus on the back-end, between the issuing bank and the acquiring bank, ensuring smooth transactions between banks.

Though some gateways offer features like virtual terminal capabilities for manual payment processing, their primary role is secure data transmission and communication with the payment processor for authorisation and settlement (A.K.A the front-end). Payment processors, on the other hand, specialise in coordinating the entire payment process with the banks.

How to choose a payment gateway for your website

Choosing a secure payment gateway is an important decision for a business, and needs to be made in a considered fashion to ensure you choose the gateway that is the best fit both for the way your customers want to pay and the profile of your business operations.

However, there are some easy key points that businesses should consider when choosing a gateway, depending on the size and maturity of the business, the industry and the target market.

Cost

Payment gateway integration – how easy is it to get set up? Will you require any development to integrate into your online shopping cart or retail facilities?

Payment gateway processing charges – this one depends on the gateway and they will either come as a monthly fee or a fixed fee per transaction.

Payment processor fees – you will also have to pay a fee to the payment processor. If it’s a card network, fees can be as high as 3%.

Interchange fees – the merchant pays them for accepting credit/debit card payments from the cardholder.

Make sure to ask about any other fees that may apply. The last thing you want to do is to commit to a solution that won’t give you a clear picture of your costs when using it.

Currencies

If you accept payments from international customers, your payment gateway should be able to provide cross-border options and be able to accept multiple currencies.

The majority of eCommerce-focused payment gateways don’t accept cryptocurrencies. If you’re also considering accepting crypto payments for your business, you will have to look for a separate gateway.

Markets

How many countries do they support around the world? If you’re a business that has a customer base outside the UK, you should keep in mind that your payment gateway should be able to accept payments from other countries as well. Here you should also consider whether a gateway provides language optimisation and local payment options.

Payment options

Generally, you should ensure you offer the payment methods that your customers prefer to reduce the chance of drop-off during the checkout process. The norm is for a payment gateway to accept and process card transactions. Still, increasingly alternative payment methods are being made available, such as bank transfers, digital wallets, vouchers and A2A payments powered by open banking (like Yaspa’s instant cardless payments).

If you have a subscription-based model, then, naturally, make sure this option is available through your chosen payment gateway.

Payment environments

In an omnichannel world, where shoppers move between multiple devices and environments, you may need to ensure your payment gateway supports both offline and online transactions. Do they also cover in-app and website payments? Can you integrate them with your electronic point-of-sale?

Security

This is often an overlooked factor when choosing a payment gateway. Since the nature of a payment gateway is to process transaction data, its systems must be robust and secure. Because when something goes wrong, the first person your customers will turn to will be you. Make sure that the payment gateways you’re looking for are PCI DSS level 1 compliant, which is the highest security level of compliance, and, if in the UK, are regulated by the Financial Conduct Authority (FCA), which is the regulatory body for financial services in the UK.

Mitigating fraud not only applies to your customers but also yourself as a merchant. Look for payment gateways that offer payment methods with inherently low fraud risk, or provide additional layers of protection from things like chargebacks or the deceptive use of another’s account resulting in “friendly-fraud”. For instance, methods built on open banking verify the account holder directly using their biometrics from within their banking app, thus avoiding the fraud that comes with card payments.

Operations

Finally, look at how your payment gateway can integrate within your existing systems and processes to ease, rather than add to, the friction of your day-to-day operations. This includes automated reports, plug-in functions, and integrations with your other software (e.g. accounting).

Using Yaspa through a payment gateway

Yaspa’s instant cardless payments use open banking technology to reduce friction at checkout, processing payments 36-times faster than cards to offer a seamless checkout experience. Not only does this mean that our A2A payments are more cost-effective, but they’re also user-experience (UX) optimised to make payment journeys intuitive, easy, and drive conversion. It takes consumers just three steps to complete a payment with Yaspa – and funds settle instantly.

For merchants, you can add Yaspa as a payment option to your online checkout process alongside existing providers. You can do this by integrating our solution directly or look out for us in your current or prospective payment gateway provider. We work with many brands, large and small, across the UK and Europe, including payment gateways and e-wallets from a variety of sectors.

And for payment gateway providers looking to meet growing customer demand for alternative payment methods, we offer integration through APIs to facilitate easy adoption and provide a streamlined payment experience for your merchant customers and their end-consumers.

Try Yaspa’s payments for yourself by making a £1 charitable donation here, and for a full demo talk to us here to learn more about adding Yaspa to your checkout. And to be the first to hear the latest updates on open banking and payment innovations, follow us on LinkedIn.

This article is a revision of one published in August 2022.

Intelligent Payments

Yaspa’s Intelligent Payments combines Pay by Bank transactions, AI-powered verification, and real-time risk assessment into a seamless, secure experience.