Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

*Updated March 2021*

Open banking has enabled a wide range of innovative financial services across the EU & the UK. Yaspa is a payment acceptance platform built using open banking, with numerous powerful features designed for the needs of companies in regulated spaces.

Open banking is the UK’s implementation of the EU’s PSD2 initiative. It aims to support the development of fintech services based on instant, consensual access to consumer bank accounts.

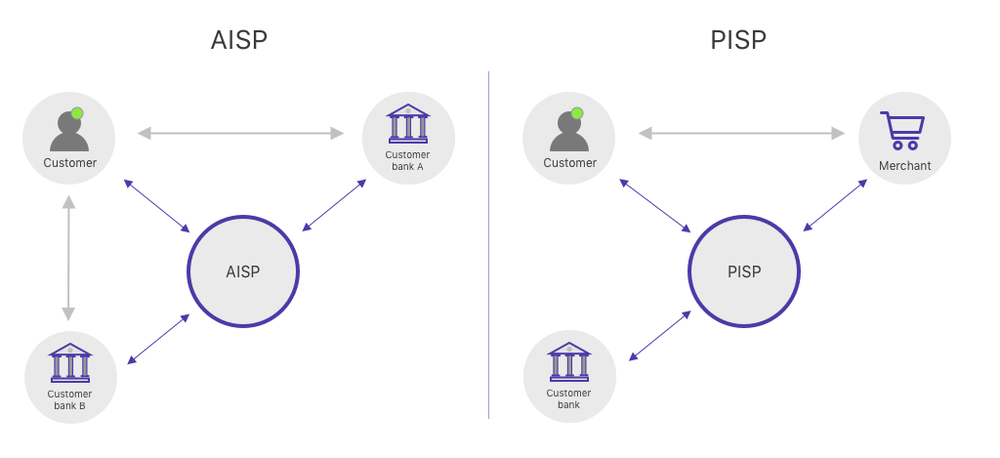

The PSD2 legislation created two service types, providing payments or account information. These are offered by Third Party Providers, or TPPs in PSD2-speak. These two services are referred to as Account Information Service Providers (AISPs) and Payment Information Service Providers (PISPs). AISPs can supply data from consumer accounts while PISPs can move payments directly from one bank account to another.

Account information services support faster and simpler forms of bank-based KYC checks, as well as confirmation of account holder identities. Working with a PISP lets you offer customers a straightforward and instant way to deposit funds that is cost-effective for you.

If you’re interested, you can learn more about open banking by following this link to an article taking a closer look at the subject. But now we’ll take a closer look at what Open banking can do for crypto exchanges.

Direct account-to-account (A2A) payments are cheaper than any other payment method. Open banking enables third-party initiation of A2A payments. Some countries already use similar methods; iDEAL in the Netherlands, BanContact in Belgium and SoFort in Germany.

Direct payments let consumers pay in seconds with no need to enter card numbers. Merchants benefit from lower payment costs as the number of parties claiming a percentage of the transaction falls.

As regulated companies, cryptocurrency exchanges need to verify the identities of their customers to a high standard. The conventional method is asking for a passport scan and selfie picture, delaying the onboarding process and frustrating the customer.

Online identity is based on layers of trust, with bank-based identity offering a more secure layer than traditional methods. Banks conduct their own KYC process at the point of account creation, checking the identity of a customer against their passport in person.

Companies can leverage AISPs’ services to significantly decrease friction during customer onboarding. Open banking requires banks to share at a minimum account number, full name and confirmation of funds. Depending on the bank, information like birthdate, address, email and phone number can be provided as well.

With the combination of bank-backed address and birthdate, exchanges can identify customers without any passport or selfie. In this case, exchanges can receive instant confirmation of funds, directly with the customers’ full name and account number.

Seamless customer onboarding is an important factor for accelerating growth on cryptocurrency exchanges. 2017’s bull run saw most exchanges struggle to cope with the number of new sign-ups. Mandatory KYC requirements have been introduced since then, increasing the difficulty of onboarding new customers. The Bitcoin run-up during the spring of 2019 saw some exchanges crash during peak trading hours. As we are approaching the next Bitcoin halving, a new bull market is likely to occur.

This opens up opportunities for exchanges to win significant market share. Exchanges need to provide a seamless customer onboarding process while maintaining compliance, especially with the market maturing and institutional money flowing in.

Open banking has created the opportunity to tie trader identities directly to payments. Bank-based identity is a secure way to let customers identify themselves on exchanges. Furthermore, account-to-account payments offer convenience for consumers and cost savings for companies.

Yaspa provides Europe-wide coverage with direct bank integrations, letting traders identify using their bank accounts and pay directly from these. These payments settle instantly and can include confirmation of account holder identity. Visit our website to learn more about Yaspa here.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields