Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

As a natural continuation of open banking, the opening up of payments and data services, open finance is designed to further enable competition in highly secure and innovative ways, benefiting both businesses and consumers.

But the difference between open finance and open banking is not entirely obvious, so in this blog, we’ll explore both in more detail, and look at how they can help businesses and consumers alike.

Open banking is the sharing of consumer data between banks and regulated third parties with the consent of the consumer. Open banking is primarily focused on payments and data. Payments via open banking technology are safer, faster and less costly than legacy alternatives, and data services enable consumers to make better informed financial choices, like credit checks and loan assessments.

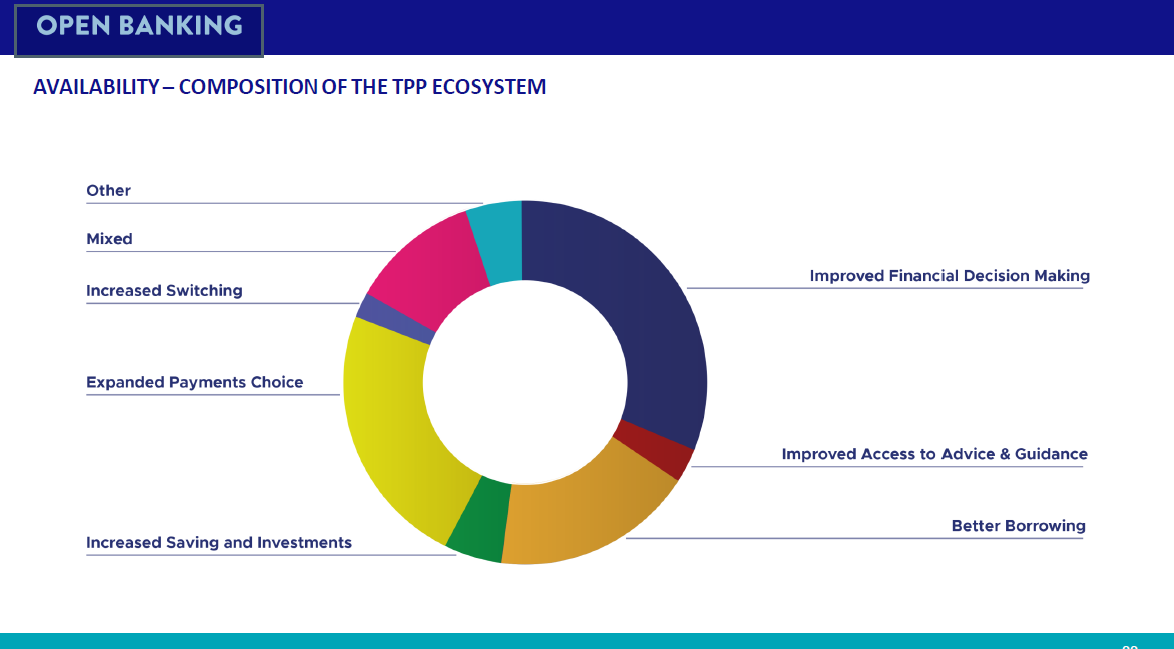

This outline shows how Third Party Providers (TPPs) are using open banking to provide a wide variety of different services to UK consumers. You can see that the ‘expanded payments choice’ delivered by services such as ours at Yaspa is a substantial component of the suite of potential open banking benefits (but very definitely not all).

Open finance is defined by the UK’s Financial Conduct Authority (FCA) as the “extension of open banking-like data sharing to a wider range of financial products, such as savings, investments, pensions and insurance”. To summarise, open finance is a range of financial products supported by open banking technology.

Though they may sound similar, open finance and open banking aren’t the same thing.

Open banking is the technology that enables previously-isolated financial information, such as your personal details and transaction data, to be shared securely between banks and payment services. Information is only shared with the explicit consent of the individual, giving consumers more control over their data. As a result, open banking simplifies account verification, enabling the fast and secure movement of funds between accounts.

Open finance is the extension of this initiative to include other financial services and products, such as mortgages, savings, and pensions, plus more accurate and fast credit checking and fairer insurance, that aims to help consumers to make better financial choices. Open finance enables a consumer’s entire financial footprint to be shared with entrusted third parties, as well as their banking information.

Just like open banking, it is envisioned that open finance will give retailers and businesses the opportunity to personalise and tailor their services more effectively, and thus increase competition in the long run. Having access to their customers’ data will help them drive value-focused solutions and build stronger brand loyalty with the consumers, positioning their individual wants and needs at the centre. Simultaneously, it will help businesses reduce costs while creating efficient solutions.

Currently, there is no regulation for open finance. However, a group of large and mid-sized fintechs have formed the Open Finance Association to develop the underlying architecture of open finance in the UK (The Fintech Times, 2022). The association is aiming to “promote a healthy and sustainable fintech framework, in which consumers and businesses all benefit from improved, innovative services”, according to the Association’s Chair, Nilixa Devlukia.

In the UK, appropriate action is being taken to set the right open finance ecosystem, with fintechs and policymakers working together. The lessons learned from open banking will make it easier to predict and understand the possible challenges and vulnerabilities associated with creating a sustainable and secure environment for the open finance industry to grow.

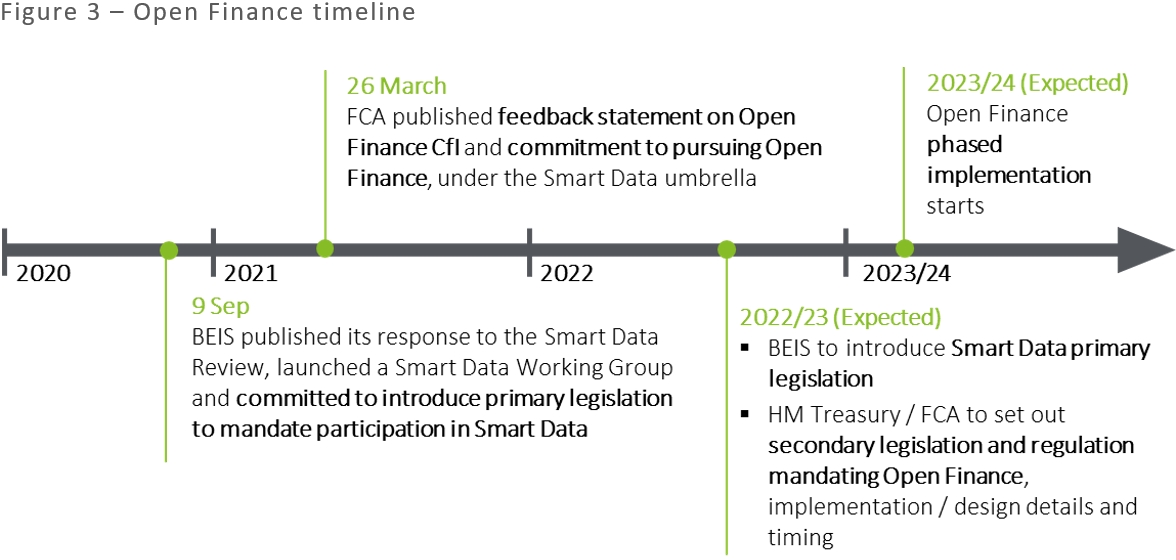

Below is the regulatory timeframe of open finance in the UK, as expected by Deloitte. We have also provided you with a mini glossary to help make the jargon less confusing.

Yaspa (a ‘TPP’) was one of the first fintech providers to offer open banking-based services in the UK. Our service enables instant cardless payments – allowing businesses of any size or type to receive and send funds that reconcile immediately, with far lower fees than debit or credit cards, and a user experience that simply delights.

Open banking is transforming the way we pay. Try it for yourself, or contact Yaspa for a demo.

Want to hear more updates from the payments and fintech world? Sign-up to our monthly newsletter to receive the latest news direct to your inbox.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

Sorry, you have reached the maximum number of form entries.