Subscribe

Stay in the know

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

The payment landscape in the Netherlands is vast and impressive. With a strong inclination towards digital payments among consumers and a robust real-time payment infrastructure already in place, it sets a solid foundation for the growth of open banking:

There’s consumer appetite for a variety of payment methods in the Netherlands, including traditional methods like debit and credit cards, and digital alternatives – which made up an 83% share of the country’s total online payments in 2022 – such as; mobile wallets; the Netherlands’ Instant Payments network, iDEAL; and SEPA Direct Debits.

Though debit cards are the method of choice for 79% of Dutch point-of-sale (offline) transactions, the uptake of digital methods and Buy Now, Pay Later (BNPL) is on the rise. Adoption of digital wallets, like Apple Pay and Google Pay, for mobile and online payments has increased in recent years, while the Dutch account-to-account (A2A) payment method, iDEAL (more on this later), accounted for 70% of all eCommerce transactions in 2022 (Statista, 2023).

The shift towards a cashless society in the Netherlands is being accelerated by the vast range of digital – and largely instant – alternatives on offer, coupled with the closure of ATMs. Just under half of the population (40%) use real-time method iDEAL as their primary way to pay, and in 2022, 85.7% of consumers used online banking and digital financial services. This implies openness and comfort with using digital and instant payment methods in the Netherlands – many may even expect to pay this way by default (Netherland Payments Market Trends).

Instant Payments, a service introduced by the Dutch Payments Association in 2019, handles almost all of the country’s non-retail payments and is the increasingly popular method for A2A credit transfers. It works with most major Dutch banks, and while it’s different to the European open banking standard called the Single Euro Payments Area (SEPA) initiative, plans are underway to make SEPA Instant Credit Transfers (SCT Inst) and Instant Payments compatible. Dutch Payment Services Providers (PSPs) already offer SCT Inst for all digital one-time transfers, rapidly making it the ‘new normal’ in payments.

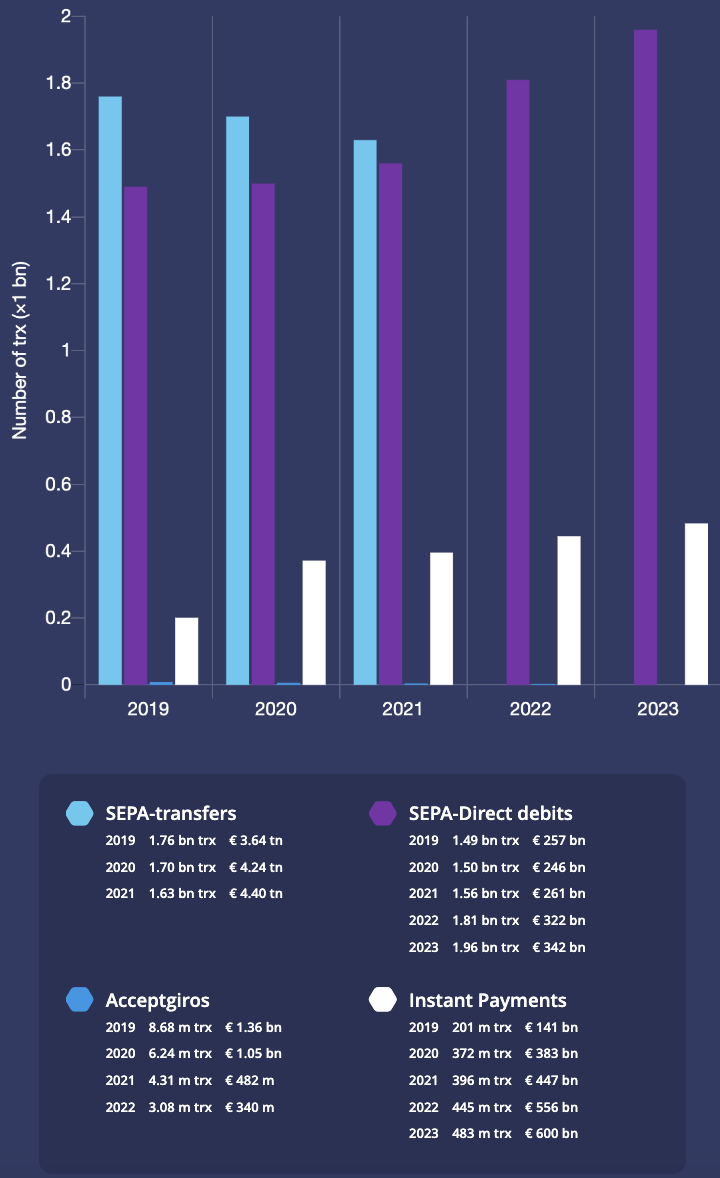

*Figures on SEPA Credit Transfers are no longer available.

**Acceptgiros was a Dutch request-to-pay on-paper provider that was phased out in 2023.

Simply put, open banking allows secure access to bank-held customer data and there are plenty of reasons to pay with it, including its ease of use, speed and security; you can read about it in more detail in our extensive article on the topic, here.

Though steady, the growth potential for open banking in the Netherlands is promising thanks to the population’s comfort with using real-time payment methods; 31% of consumers expressed an openness to using services facilitated by it (Four European takes on open banking, 2023).

Legislation is also paving the way for an uptick in open banking users across the Netherlands. In February 2024, the European Parliament announced the regulation of instant payments across Europe; all transactions within the Eurozone will take less than 10 seconds, and the regulation of real-time payment infrastructures will be standardised. This is significant to open banking’s success in the Netherlands; it will force the country’s SEPA Instant Credit Transfer (SCT Inst) providers like banks and payment providers to all adopt the same, pan-European open banking standards. Dutch banks will be obligated to standardise the way they manage and send payment outcomes (e.g. whether a bank has accepted or rejected a payment) to merchants using open banking payment services, which has varied significantly in the past. Standardisation will improve clarity and security for merchants, and we can also expect to see merchant adoption of open banking payments grow, particularly in sectors outside of retail, like iGaming, where iDEAL is not widely used.

The accommodation of SEPA for open banking in the Netherlands will also bring benefits such as greater access to bank account information (which has so far been limited) via the SEPA Payment Account Access (SPAA) scheme. This will include account holder attributes like date of birth – a game-changer for age-regulated industries in the country. The scheme will also fast-track the application of open banking-powered recurring payments (VRPs) – a capability iDEAL’s technology can’t provide – perfect for subscription businesses like Dutch lotteries or utilities.

Launched in 2005 by a consortium of Dutch banks, iDEAL has become a popular real-time payment method for online retail transactions in the Netherlands and often considered the country’s forerunner to open banking. Like open banking, iDEAL enables a person to send funds directly from their bank without a card for payments that are fast and 2FA secure. SEPA, however, uses purpose-built payment infrastructure to transfer funds between accounts instantly – these are called payment rails and you can read about them in our blog on the topic, here. It’s this familiarity with real-time payments that’s paving the way for the widespread adoption of open banking payment services in the Netherlands. However, they do have their differences:

The variety of payment options in the Netherlands, and the reason open banking is likely to thrive there, is also the reason open banking is yet to be more widely adopted. Methods like iDEAL and the Dutch Payments Association’s Instant Payments service have dominated the market for many years, earning a sense of familiarity and trust among the Dutch population. Like open banking in the UK, adoption challenges sit on the consumer side: there are many providers of open banking services but no universally recognised symbol or messaging. However, Dutch aptitude for digital payment methods means many consumers are comfortable sharing their financial data with third parties – 25% expressed no concerns at all – creating a promising catalyst for future open banking adoption in the Dutch market (Four European takes on open banking, 2023).

The standardisation of instant payments will make a big impact on overcoming the challenge of disparate payment handling processes by the banks in the Netherlands. Soon, all Dutch banks will have to process IBANs belonging to providers from outside of the country and expand their SCT Inst offering. This will make open banking much more appealing for those looking to purchase and accept payment instantly for goods and services from outside of the Netherlands.

The state of open banking in the Netherlands reflects a landscape that is primed for its adoption. The payment ecosystem is diverse and forward-thinking, with open banking playing a pivotal role in the harmonisation and elevation of financial and payment solutions. As regulation continues to be rolled out across Europe, the Netherlands’ journey to open banking promises to be an exciting one.

Yaspa is at the forefront of the open banking revolution. We offer a wide range of services including; account verification; A2A payments across Europe; vIBANs, and more, to give businesses in the Netherlands:

If you’re interested in learning more about what Yaspa can do for your business, do get in touch. We would love to hear from you.

Subscribe

Discover the latest payments news and events from Yaspa and the fintech world in our monthly newsletter.

"*" indicates required fields